India’s economic performance for January 2023 reflected diverse trends, featuring a slowdown in 9exports, manufacturing, and services activities, and higher inflation, but positive movements in demand indicators, GST collections, rail freight volumes, and jobs. Overall, India’s economic recovery continues but at a relatively slower pace than in the previous month.

The Reserve Bank of India (RBI), which has raised borrowing costs six times since May, is expected to increase interest rates again in its April review amid inflation exceeding estimates and global central banks tightening further.

Retail activity in January 2023 continued to improve on the back of the festival/wedding season, with sales value gains of 16% over the corresponding pre-Covid period of 2019. On the supply side, the Markit Purchasing Managers’ Indices (PMI) for Manufacturing and Services both dropped slightly.. The overall unemployment rate in January also dropped, albeit with better labor participation in urban areas. Goods and Services Tax (GST) and rail freight revenues were steady in tandem with the market activities and increased compliance, and capital expenditure was up from the previous month.

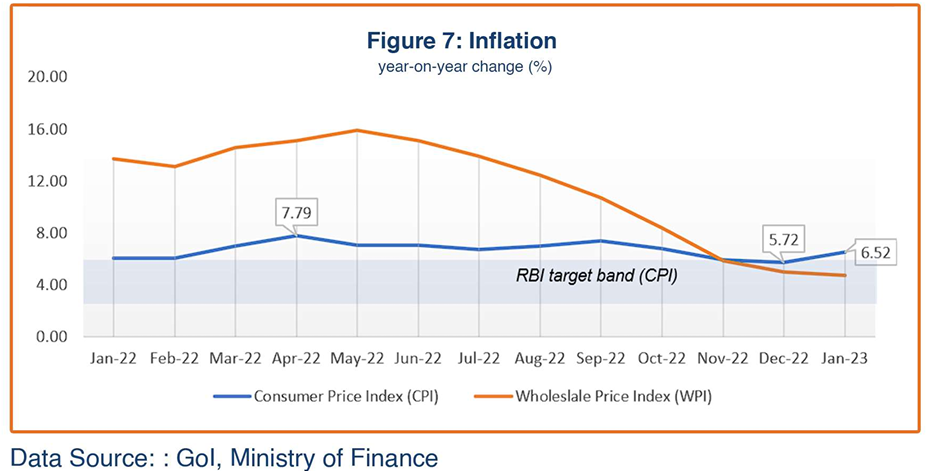

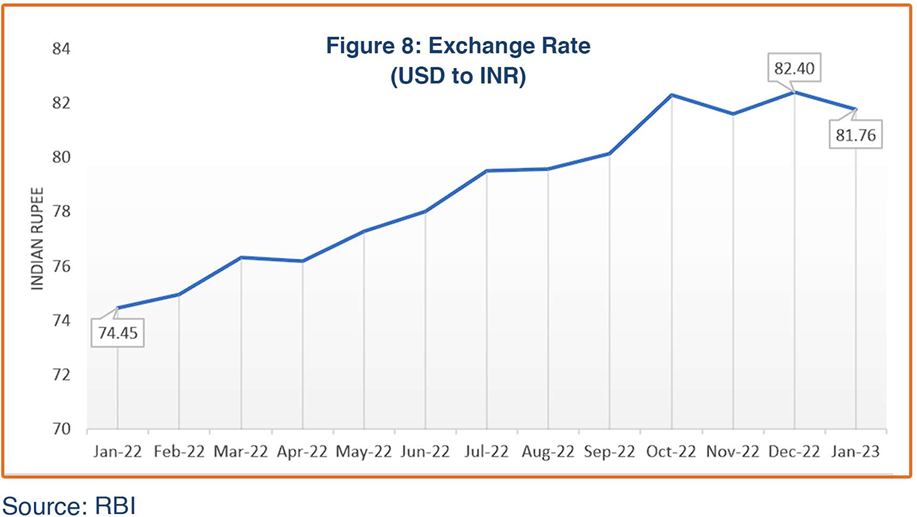

As anticipated, currently facing a volatile global recession, India’s exports decelerated in January 2023 while imports fell even more sharply. As a result, the trade deficit was down significantly in January. At the same time, net FDI flows recovered in December 2022 from a net outflow recorded in the previous month (latest available). India’s foreign exchange reserves improved to $575 billion in January end and the Indian Rupee recovered to an average of 81.76 against the US Dollar, from 82.40 in the previous month. CPI inflation rose to 6.5% in January 2023, after remaining within the RBI safety band of 2%-6% for the previous two months, led by higher food prices; core inflation also rose beyond 6%. The wholesale price index (WPI), in contrast, dropped to 4.7% in January, maintaining its downward trajectory for the last eight months.

India recorded an impressive cumulative growth of 9.6% during the first six months of FY2022-23. The RBI has forecasted 4.4% growth for the third quarter of IFY2022-23 (October-December 2022), on the back of a strong performance in the agriculture and services sectors. Growth in the manufacturing sector has been uneven throughout the first ten months of the current fiscal year.

The Government of India presented its Union Budget FY2023-24 on February 1, focused on enhanced capital expenditure, which it hopes will attract private investments. With a resilient financial system, a growing services and agriculture economy that drives a strong demand, and an emphasis on infrastructure development, India’s growth outlook appears bright in the long term. However, an uneven recovery in its manufacturing sector and uncertainty in the exports sector may dent India’s economic growth prospects in the short term.

Demand Recovery Trends

Retail sales in January 2023 showed an uptrend in consumption demand. Vehicle sales were up significantly, by almost 27% from the previous month, depicting sustained consumer sentiment despite higher auto loan costs. The RBI reported healthy bank credit growth at 16.3% at the end of January, compared with 14.9% a month ago, even though the cost of credit remains high due to liquidity tightening. The Retailers Association of India (RAI) survey reported 16% higher sales during December 2022 compared to the pre-pandemic sales recorded for December 2019, and retailers reported higher sales for apparel, home decor, beauty, personal care, quick service restaurants, footwear, food, and grocery. The sustained, reasonable rise in retail sales during the first ten months of the current IFY2022-23 suggests domestic demand will drive overall economic growth for the year.

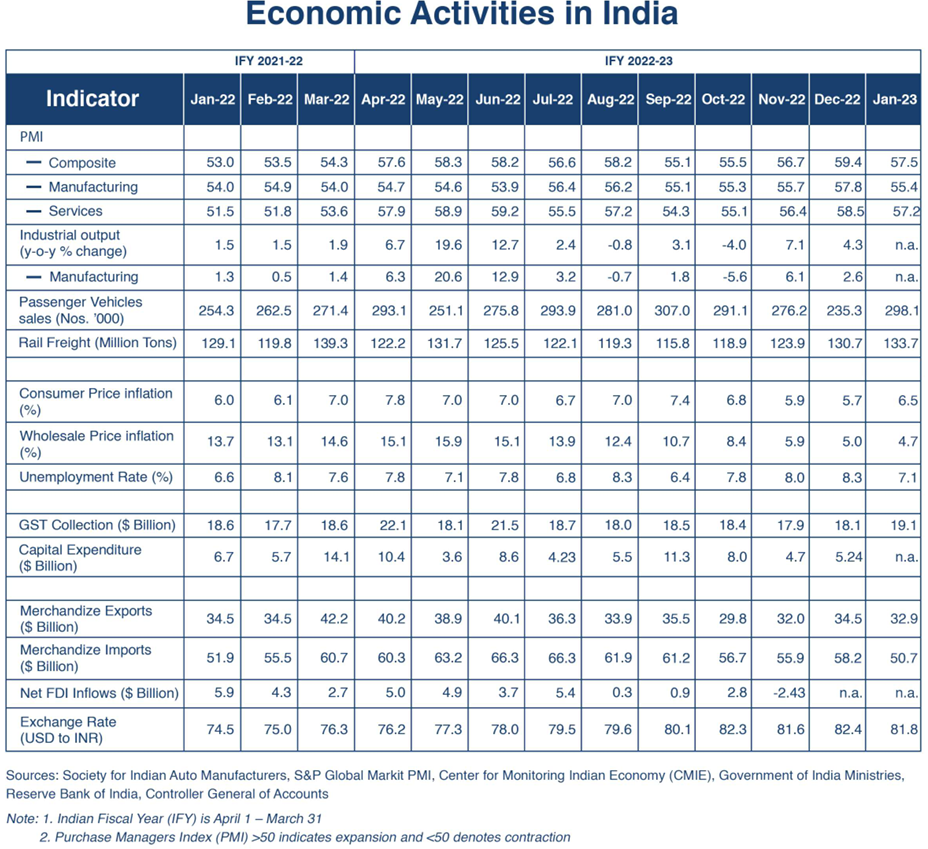

GST Revenues

Goods and Services Tax (GST) collections have ranged between $18.0 and $18.5 billion per month since July 2022.. In January 2023, GST collections are estimated at $19.1 billion, up from $18.1 billion the previous month, an indication of improved consumer spending (Figure 1). Analysts note that rising GST collections reflect a combination of increased economic activity, increased tax rates, and increased compliance.

Supply Side Dynamics

Supply Side Dynamics

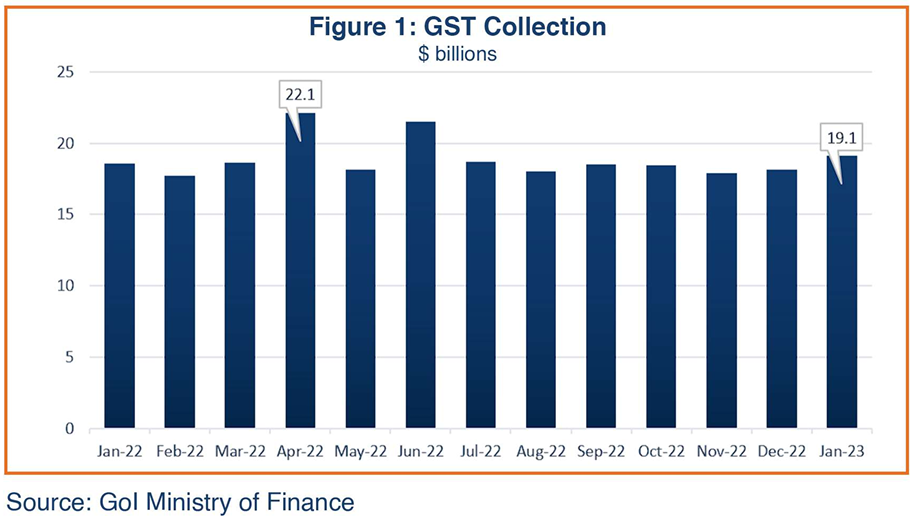

Overall business sentiment in January 2023 was slightly lower than that in the previous month, with the Composite Markit Purchase Managers Index (PMI) falling to 57.5 from the peak of 59.4 recorded in December 2022, indicating slower expansion in manufacturing and services activities (Figure 2; a PMI above 50 reflects the optimistic mood of businesses that have made bold input purchases in anticipation of increased demand.) The Services index declined to 57.2 from 58.5, and the Manufacturing index fell to 55.4 from December’s 57.8.

Overall business sentiment in January 2023 was slightly lower than that in the previous month, with the Composite Markit Purchase Managers Index (PMI) falling to 57.5 from the peak of 59.4 recorded in December 2022, indicating slower expansion in manufacturing and services activities (Figure 2; a PMI above 50 reflects the optimistic mood of businesses that have made bold input purchases in anticipation of increased demand.) The Services index declined to 57.2 from 58.5, and the Manufacturing index fell to 55.4 from December’s 57.8.

Industrial Production

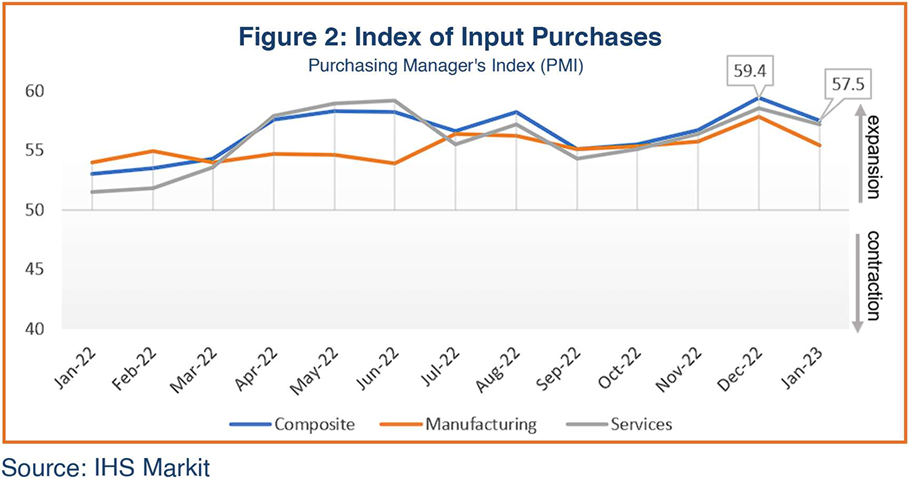

India’s industrial production growth on a year-on-year (y-o-y) basis eased to 4.3% in December 2022 from an upwardly revised 7.3% in November. Increases in industrial production were led by electricity, mining, and manufacturing output (Figure 3). Growth across all segments recovered compared to the previous month, generating an acceleration in overall industrial output growth. Manufacturing, which accounts for 77% of total industrial production, recorded 2.6% growth, compared with an upwardly revised 6.4% growth in November; mining output growth, which comprises 14% of total industrial output, at 9.8% was marginally up from 9.7% in the previous month; and the growth rate in electricity production (8% of total industrial production) was impressive at 10.4%, but less than the 18% recorded in the previous month. Capital goods production within the manufacturing sector showed 7.6% growth in December, suggesting reasonable growth in investments. The trajectory of industrial output throughout the year has remained erratic, suggesting an uneven recovery, and reflecting the impact of persistent supply chain disruptions.

Trade

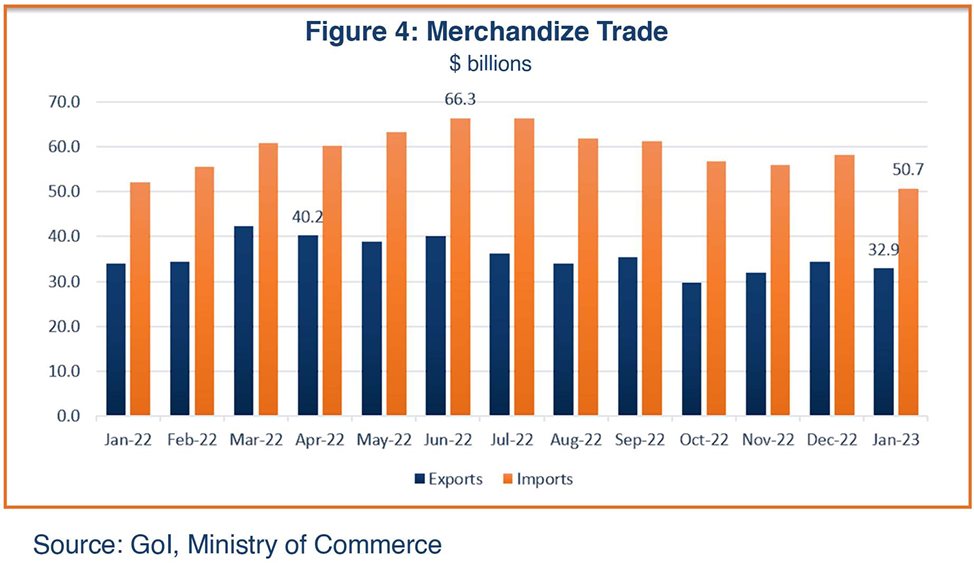

India’s merchandize exports dipped 4.6% in January 2023 to $32.9 billion from the previous month’s $34.5 billion (Figure 4). Export performance in the first quarter of the current fiscal year was robust but slowed in the second and third quarters. India’s exports in January 2023 performed well in commodity groups, such as electronic goods, petroleum products, and chemicals, while export sales were down for iron ore, gems and jewelry, iron and steel engineering items, and cotton.

India’s merchandize imports, at $50.7 billion in January 2023, were 13% less than the December purchases of $58.2 billion, easing pressure on India’s current account balance. India remains a major importer of fuel to meet its increasing domestic demand. In the third quarter of IFY2022-23 (October-December 2022), imports moderated due to lower commodity prices, helping India’s merchandize trade deficit to narrow.

A sharper slowdown in imports than that in exports in January 2023 led the reduction in India’s trade deficit to nearly $17.8 billion from $23.76 billion in the previous month.

Government Capital Expenditure

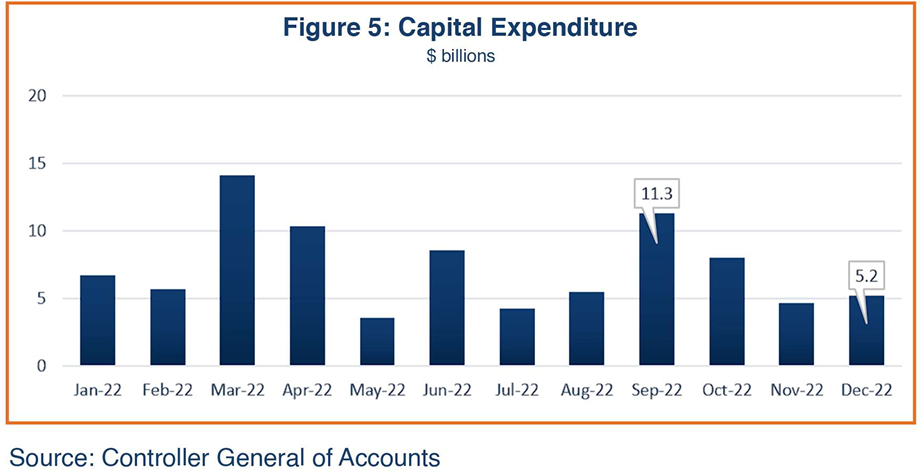

Capital expenditure growth has been uneven for the entire fiscal year 2022-23 so far (April-December 2022 -Figure 5). The finance minister expects to meet the fiscal deficit target of 6.4% of GDP in 2022-23, which is a much lower deficit than the 9.3% recorded in the previous two COVID years. Though the government is faced with the challenges of low privatization receipts and expenditure pressures, it is still expected to trim the fiscal deficit target to less than 6% in its budget for the next fiscal year (2023-24). The finance minister in the Budget 2023-24 speech reiterated the goal of lowering the fiscal deficit below 4.5% of GDP by FY2025-26.

Foreign Direct Investment (FDI)

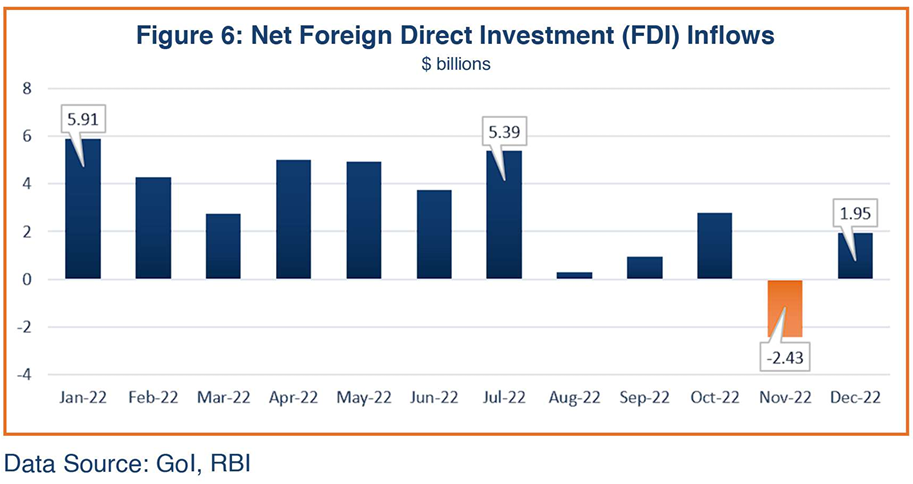

Foreign direct investment (FDI) equity flows showed mixed trends throughout the fiscal year 2022-23. Net FDI inflows peaked in the current fiscal year in July at $5.39 billion, after which flows reversed drastically, becoming a $2.4 billion net outflow in November (Figure 6 – latest available data); however, a recovery in December 2022 brought up the net inflows to $1.95 billion. The nodal Ministry of the Gol has attributed the downtrend in FDI inflows to a relatively weaker sentiment in the investing community facing headwinds of the geopolitical tensions and the economic slowdown.

Inflation

Consumer Price Index (CPI) inflation was 6.5% in January 2023, up from 5.7% in December 2022, again crossing the RBI’s target ceiling of 6.0%. Retail inflation in India had stayed within the RBI safety band of 2%-6% for two consecutive months starting in November (Figure 7), then rose in January mainly due to a more than expected increase in food prices, which account for about 40% of the CPI total; core (non-food) inflation also remained high at 6.3%. The RBI continues to monitor prices, stating it projects inflation to remain above 4% for the majority of 2023. The RBI has raised the benchmark repo rate by 250 basis points since May to 6.5%. Economists expect further tightening in RBI’s monetary policy in April 2023.

Wholesale Price inflation in January 2023 dropped further to 4.7% from 4.9% in December 2022, the lowest level in two years. India’s WPI inflation has been declining steadily for the last eight months. Business sentiment is expected to improve following further easing of wholesale input prices.

Foreign Exchange

India’s foreign exchange reserves were $575 billion at the end of January 2023, gaining approximately $12 billion from December. The RBI intervenes intermittently in the foreign exchange market for liquidity management, including the selling of dollars, to manage depreciation in the rupee, which can impact exchange reserves. Foreign capital inflows and falling international prices have contributed to the gains in foreign exchange reserves and slight appreciation of the Indian Rupee (INR). The INR touched its weakest level, 82.78/USD, on January 4, but the average monthly exchange rate for January recovered to 81.76/USD from the previous month’s 82.40/USD (Figure 8).

Economic Outlook

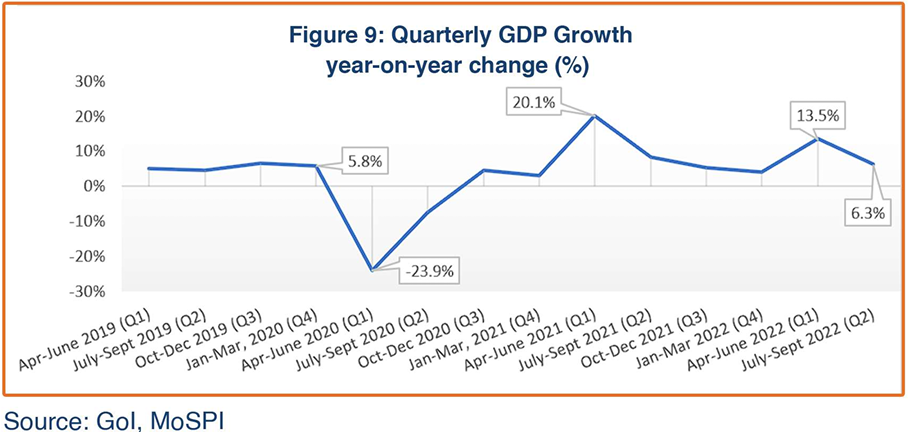

India’s GDP growth rate in the second quarter (July-September 2022) slowed to 6.3% from 8.4% in the corresponding period of the previous year (Figure 10). The RBI in its recent monetary policy statement noted the near-term growth outlook remains weaker than previously expected. It has revised its forecast for GDP growth in the current fiscal year down to 6.8%, in line with the IMF’s forecast, reflecting extended geopolitical tensions and continuing aggressive monetary policy tightening globally. However, the World Bank has recently made an upward revision in its 2022-23 growth forecast for India, to 6.9% from 6.5% previously, on account of stronger consumption and increased domestic economic activity.

While the services and agriculture sectors continue to enjoy recovery, industrial and manufacturing output have shown a limping growth pattern during the first ten months of the current fiscal year. Continuing volatility in global inflation, as well as uncertain export orders, will likely make a significant difference in the performance of the economy and India’s growth outlook in coming months.

The Union Budget for IFY2023-24, presented on February 1, 2023, featured a significant increase in capital expenditures to 3.3% of GDP (an increment of 0.6% compared to the IFY2022-23 level) to support infrastructure-led economic growth and private investment. The ratio of capital spending to revenue expenditure peaked at 28.6%, the highest level in two decades. The enhanced capital expenditure underscores the government’s focus on supply-side rather than demand-side support. Furthermore, the government hopes its enhanced capital expenditure will crowd in greater private investment, strengthening demand and raising India’s baseline growth potential.

Expecting an easing of crude oil prices to average $95 per barrel for the year, the RBI revised its inflation projections for the current fiscal year to 6.5% from the earlier 6.8%. The outlook for inflation remains uncertain owing to the risks of supply disruptions from continuing geopolitical tensions.

Sustained credit growth, a resilient financial sector, and the government’s continued thrust on capital expenditure imply an investment-friendly climate that should push India’s economic growth in the next fiscal year; however, India’s export may continue to be lackluster if the global slowdown prolongs, which would in turn hobble faster GDP growth.