India’s economic outlook remains volatile due to the impact of continuing uncertain geopolitical shocks, global recession and rising prices. Nevertheless, the economy has shown some resilience and consumer spending and demand have continued to show positive trends in the month of October 2022. Industrial output and urban employment also improved during October, but the trade deficit ballooned due to plunging exports. The Indian currency also plummeted to its historic lowest level against the dollar. Retail inflation was also down, though, which may help restore investors’ confidence in the Reserve Bank of India’s (RBI) monetary policy measures.

Retail activity has shown improvement on the back of demand revival during the festival season, and retail businesses reported sales value gained 19% over the pre-Covid October 2019 value. On the supply side, the Markit Purchasing Managers’ Indices (PMI) for Manufacturing improved marginally to 55.3 and the PMI for Services also moved upwards to 55.1 from the previous month. The Composite PMI was up from September due to improved industrial activities and revival in construction and mining activities. The overall unemployment rate rose to 7.8% from the previous month’s 6.4%, mainly due to the increase in seasonal rural unemployment, but factories in the service sector increased employment in October. Goods and Services Tax (GST) collections were steady in tandem with the increased market activities during the festival season, increased rates and increased compliance.

With India’s increased integration with the global markets, its export sector performance is currently reflecting volatility due to the depressed demand from most advanced countries. Exports in October tumbled 16% and imports dropped 7% from the previous month, leaving a significant negative gap in the trade balance, a major concern among India’s policymakers. FDI equity inflows in August 2022 (latest available data) slumped significantly from the previous month. India’s foreign exchange reserves, though still reasonably high, have been affected by macroeconomic uncertainties, slipping to $530 billion by October-end, while the Indian rupee depreciated about 2.7% against the US dollar to 83 from the previous month.

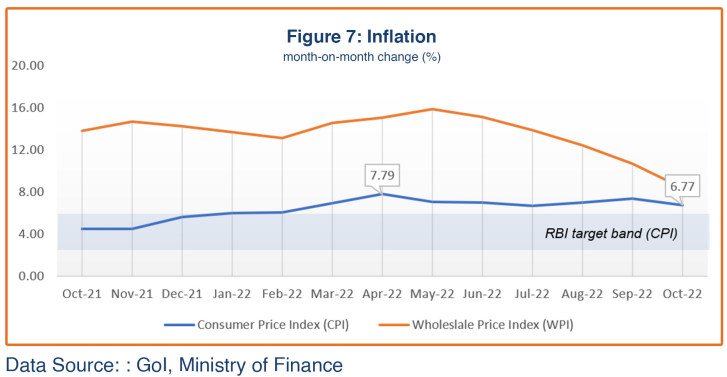

Lower food prices led a drop in the consumer price index (CPI) to 6.77% in October 2022 from the previous month’s 7.4%. The CPI is still above the RBI target ceiling of 6.0% albeit under control compared with other major economies. The RBI has kept its forecast of 6.7% retail inflation for the fiscal year 2022-23 due to the persisting food price pressures and global risks to costlier imports. The wholesale price index (WPI) dropped to its lowest level this fiscal year, 8.39% in October from 10.7% in the previous month. The smaller gap between the CPI and WPI is expected to further help reduce retail inflation.

While India has shown reasonable resilience to recent supply disruptions, its near term economic growth outlook remains unpredictable due to continuing uncertainties in geopolitical tensions and toughening global trade conditions amid rising inflation, recession, and unstable currencies. But against the backdrop of ongoing structural reforms by the government, the longer term prospects appear strong. Considering the continuing global concerns that may impact the performance in subsequent quarter, the RBI has revised India’s FY2022-23 GDP growth to 7% from its earlier projection of 7.2%. The International Monetary Fund (IMF) has also cut its economic growth forecast for India to 6.8% in IFY 2022-23 on account of extended geopolitical tensions and an aggressive monetary policy tightening globally.

Demand Recovery Trends

The festive season in India is well known to rack up one the best sales results in the year. Accordingly, retail sales in October 2022 showed an uptrend in consumption demand, though vehicle sales were down 5% from the previous month due to the impact of supply constraints. RBI reported bank credit growing 17% at the end of October, compared with 16.4% a month ago, pointing to the rising trend in demand. The monthly survey by the Retailers Association of India (RAI) reported 19% higher sales during October compared to the pre-pandemic sales recorded for October 2019. With easing consumer inflation, retailers reported higher sales for consumer durables/electronics as well as for hotel and restaurant sales. A sustained rise in retail sales and passenger vehicle sales during the first seven months of the current fiscal year depicts rising consumer demand ingraining the Indian economy, which will likely have a multiplier effect on the overall economic growth of India.

Supply Side Dynamics

Input Purchases

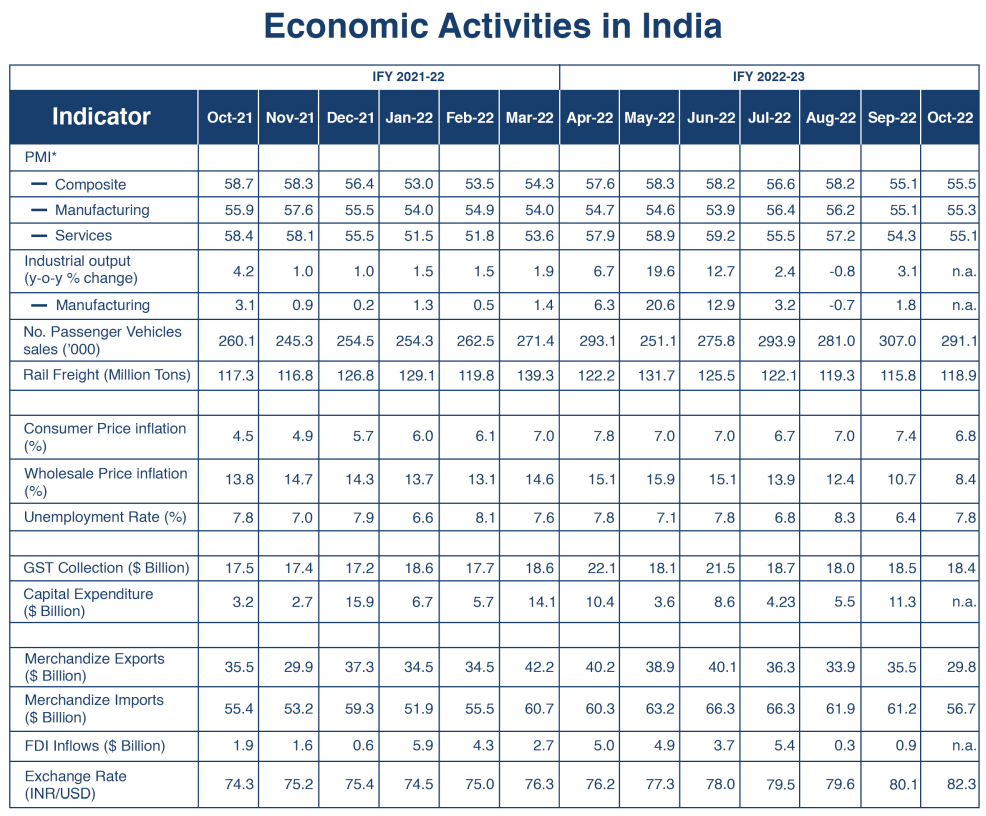

The overall business sentiment in October 2022 was stronger than the previous month. The Composite Markit Purchase Managers Index (PMI) revived to 55.5 from 55.1 in September, reaffirming the expanding economic activities (Figure 1). A PMI above 50 reflects the optimistic mood of businesses that have made bold input purchases in anticipation of increased demand. The Services index bolstered to 55.1 from 54.3 and the Manufacturing PMI index was marginally up to 55.3 from the previous month’s 55.1, implying that the service economy grew more than the manufacturing sector. According to S&P Global, new orders growth was at a two-month high, as factory orders expanded faster than sales at service providers. The S&P Global India Manufacturing PMI showed that job creation in October grew at the fastest pace in three years, with manufacturers optimistic about demand buoyancy going forward. The Employment Outlook Report for Q3 also asserts the overall intent to hire within urban players (both manufacturing and services) has increased from 61% in Q2 to 65% in Q3, but the overall unemployment rate increased in October due to an increase in seasonal unemployment in rural areas.

Industrial Production

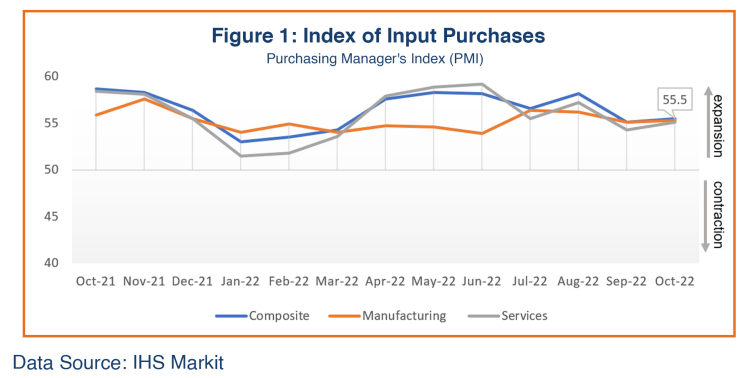

Total industrial production exceeded market expectations of 2% growth, expanding 3.1% in September 2022 compared to the corresponding period of last year, reversing the previous month’s -0.8% growth. Growth across all segments got stronger compared to the previous month, generating an acceleration in the overall growth in industrial output. Manufacturing, which accounts for 77% of total industrial production, rebounded 1.8% year-on-year in September from the decline of 0.5% of the previous month; mining, which comprises 14% of total industrial output, rose 4.6% compared with the growth of 3.9% year-on-year in August, and the growth rate in electricity production (8% of total industrial production), at 11.6%, was significantly up from the 1.4% growth achieved in the previous month. Capital goods production within the manufacturing sector showed a 10.3% growth in September 2022, hinting at remarkable growth in investments, where the rate of growth was more than double the 5% of the previous month.

A rise in industrial production growth is indicative of positive strides in India’s economic recovery, but unfavorable geopolitical trends hobble the sustainability in growth, causing ups and downs in the growth curve. A lackluster industrial output in August 2022 reflected the impact of a slowdown in global growth that is being felt by domestic manufacturing companies. That output, however, rebounded somewhat in September on increased domestic demand.

GST Revenues

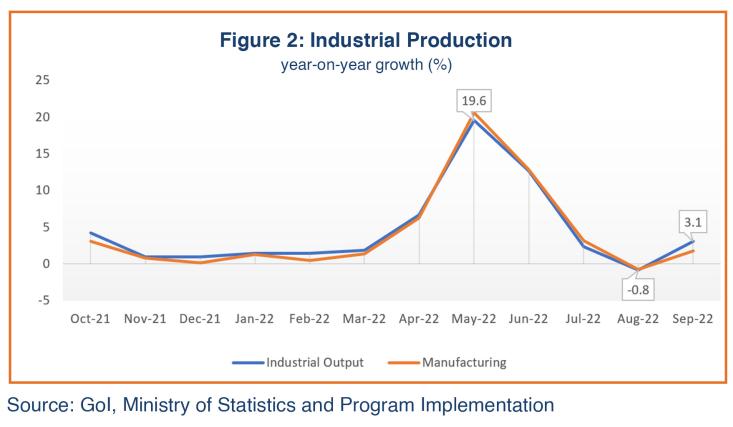

Changes in the value of Goods and Services Tax (GST) collection are an indicator of business transactions and increased tax compliance. The GST collections have been ranging between $18 and $18.5 billion since the beginning of second quarter of the current fiscal year 2022-23. The GST collections for October 2022 were $18.4 billion (Figure 3), reflective of sustained economic activities, increased rates, and increased compliance.

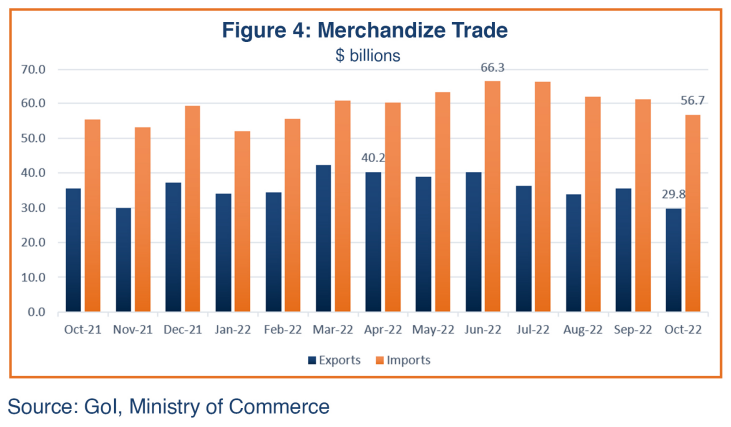

Trade

India’s merchandize exports value fell almost 16% in October 2022 to $29.8 billion from the previous month’s $35.4 billion (Figure 4); it is the lowest level since February 2021. India’s export performance until June this year was outstanding. However, the global recession, tightening of liquidity by major economies to tame inflation, currency volatility, and suppressed demand have impacted global trade negatively. As expected, India’s exports in October reflected the impact of the global economic slowdown, with a deceleration in exports of engineering items, petroleum products, ready-made garments, marine products, and chemicals and pharmaceuticals. However, exports of electronics, oil seeds, oil meals, tobacco, tea, and rice rose in October.

India’s merchandize imports are estimated to be around $61.2 billion in October, declining marginally from $61.9 billion in the previous month. With exports slowing deeper than imports, the merchandize trade deficit swelled to $31.4 billion in October from $25.7 billion in the previous month. India’s huge trade deficit continues to remain a cause of concern as it is a major component in the country’s current account deficit (CAD) and it can impact the macroeconomic balance, putting pressure on the value of domestic currency.

India recently allowed INR in international trade settlements, which is a major step to facilitate trade with Russia, Iran, Bangladesh and Sri Lanka. India continues to restrict exports of steel and iron ore pallets and their exports were negligible. (India in May raised the export tax on low-grade iron ore lumps and fines – with iron content below 58% – to 50% from zero, and hiked the duties on pellets to 45% from zero, in a bid to meet rising local demand).

Government Spending

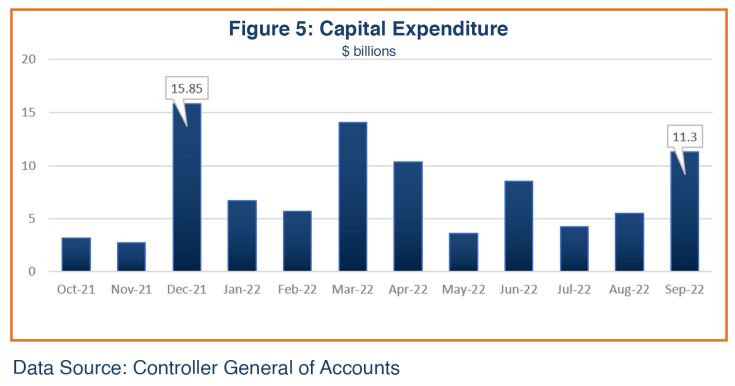

Capital expenditure growth has been moderating since the beginning of the current fiscal year, though an uptick was visible in September (Figure 5). Finance Ministry officials have stated that the government will meet the fiscal deficit target of 6.4% of GDP in 2022-23 without having to cut capital expenditure, and the government has repeatedly stressed its goal of boosting capital expenditure while controlling revenue expenditure.

Foreign Direct Investment (FDI)

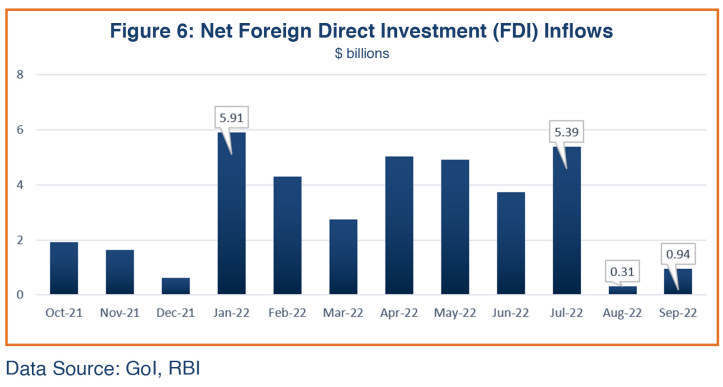

Foreign direct investment (FDI) equity flows showed mixed trends throughout the previous fiscal year. According to the latest data released by the Department of Industrial Policy and Internal Trade (DPIIT), in FY2021-22, FDI equity contracted marginally, by 1%, to $58.8 billion. However, total foreign direct investment (including equity inflows, reinvested earnings, and other capital) into India rose by 2%, peaking at $83.7 billion in 2021-22.

The first month of the new fiscal 2022-23 (April 2022) witnessed India attracting $5 billion in total FDI inflows, followed by an $4.92 billion in May and $3.74 billion in June. Net FDI inflows in July peaked to $5.39 billion in the current fiscal, just before falling significantly in August and September (Figure 5). Total net FDI inflows into India expanded more than 17% to $13.61 billion in the first quarter of FY2022-23 compared to $11.55 billion for the corresponding period of the previous year.

Inflation

The overall inflation trajectory remains volatile given continuing uncertainties in international commodity prices. The consumer price index (CPI) was several notches down to 6.77% in October 2022 from 7.4% recorded in September yet remained above the RBI’s target band of 2-6.0% for the tenth month in a row (Figure 6). The drop in CPI was mainly due to a more-than-expected fall in food prices, which comprise about 40% of the country’s CPI. Despite the continuing supply chain disruptions owing to ongoing geopolitical factors, food prices were lower due to the usual seasonal changes in food prices. The RBI continues to give priority to price stability by raising the benchmark policy repo rate; it has raised the benchmark repo rate by 190 basis points since May to 5.9%, aiming to curb consumer demand. The RBI expects inflation to remain elevated above its 6% threshold in the second half of the fiscal year despite the fall in global oil prices, which has been offset by a soaring dollar that has gained almost 12% against the rupee this year.

Wholesale Price inflation further moderated to 8.39% in October from 10.7% in September, the lowest level in about two years, mainly due to a broad-based growth in manufacturing and services. Business sentiment is expected to improve following the softening of input prices. The RBI has flagged that the narrowing gap between wholesale and retail inflation implies a lower magnitude of pass-through of input costs on future retail inflation.

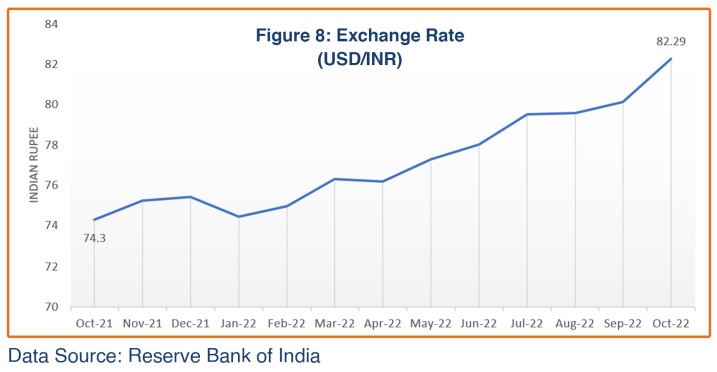

Foreign Exchange

India’s foreign reserves were $530 billion at the end of October 2022. The rupee again crossed the peak of 80.14/USD in September 2022. Persistent foreign fund outflows from capital markets, however, boosted the local currency. The average monthly exchange rate for September was INR 80.14/USD (Figure 8). The rupee has lost nearly 12% against the US Dollar since January, mainly due to a rise in global crude oil prices, tightening monetary policies globally, a strengthening dollar post Russia-Ukraine war and continuing foreign capital outflows from India. The RBI in June 2022 announced its decision to allow global trade in rupees; that may help increase foreign exchange inflows and stabilize the rupee in future.

Economic Outlook

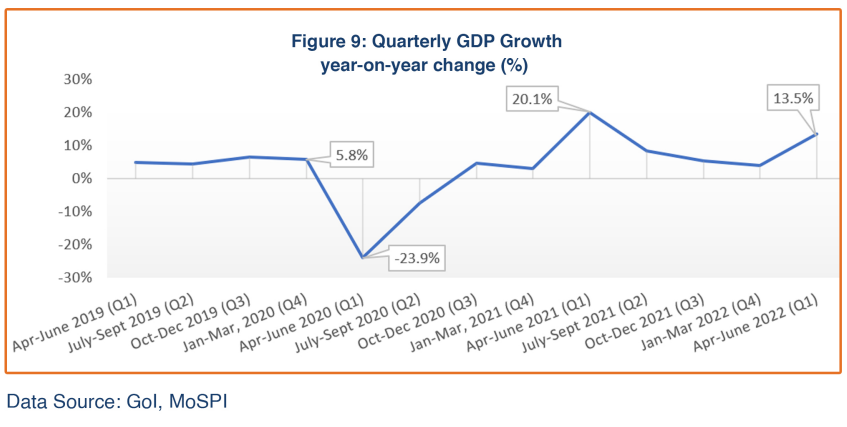

India posted 13.5% growth for April-June 2022 according to the latest government statistics. Businesses ramped up capacity as domestic demand continued to recover during the second quarter of fiscal year 2022-23. The agriculture and services sectors continue to support GDP growth and healthy improvements have been reported in important indicators, like aggregate demand, lower input inflation, private consumption expenditure, private capital expenditure and government expenditure. However, trade has been impacted by geopolitical changes, high commodity prices, and a weaker rupee. Economists project India’s economic growth will likely slow to somewhere in the range of 6.3-6.5% in the second quarter largely due to the high base and erosion of corporate profitability due to persisting inflation.

The RBI has revised its forecast for FY2022-23 GDP growth to 7.0% from the earlier 7.2% based on the continuing geopolitical challenges, such as supply chain uncertainties, global recession and the ongoing Russia-Ukraine conflict. Likewise, the IMF has also announced a downward revision in India’s GDP growth forecast for fiscal 2022-23, to 6.8%, on account of extended geopolitical tensions and an aggressive monetary policy tightening globally.

Businesses had hoped that softening international prices of fuel, fertilizers, and edible oils would help increase their profitability; however, the high input prices throughout the year proved to be a dampener. Now the narrowing gap between input and consumer prices will likely send positive signals to the business community and lift both demand sentiment and output levels. Industrial and manufacturing activities have sustained on the positive trajectory and capital expenditure is also rising. However, the falling value of the rupee against the dollar and the continuing volatility in global inflation management, as well as slumping exports, will likely make a significant difference in the performance of the economy.

Major economies around the world, including India, face challenges of currency depreciation and the impact of global recession but Indian policymakers have voiced their confidence in India’s relatively stronger financial sectors, rising private capital expenditure, better control on inflation, and reviving foreign exchange reserves. Nonetheless, India’s economic growth outlook continues to remain uncertain currently and will be influenced by how much private investment expenditure is incurred and the magnitude of global recession.