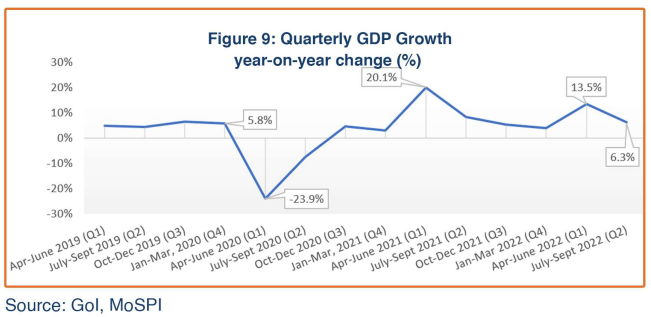

India’s economic performance for November 2022 was mixed, with encouraging signs in demand and input purchases and monetary indicators that improved due to prudent interventions by the Reserve Bank of India (RBI). However, poor industrial output in October, an increase in urban unemployment, and a significant trade deficit in November were alarming signals for the policymakers. Nevertheless, the Indian economy continues on its post-COVID growth path, posting 6.3% growth for the second quarter of fiscal year 2022-23 (July-September 2022), comparted to 8.4% in the corresponding period the previous year.

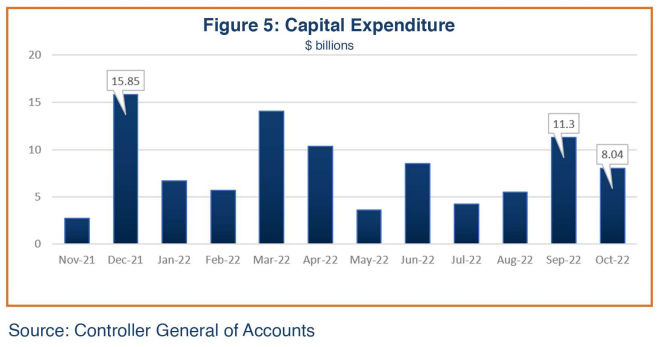

Retail activity in November 2022 showed an improvement during the festival and wedding season, with sales value gains of 15% over the corresponding pre-Covid 2019 period. On the supply side, the Markit Purchasing Managers’ Indices (PMI) for Manufacturing improved to 55.7 and the PMI for Services rose to 56.4. The overall unemployment rate in November rose to 8% from the previous month’s 7.8%, due to a significant rise in urban unemployment. Goods and Services Tax (GST) revenues were steady in tandem with market activities and increased compliance, but capital expenditure was down to $8 billion from $11.3 billion in the previous month.

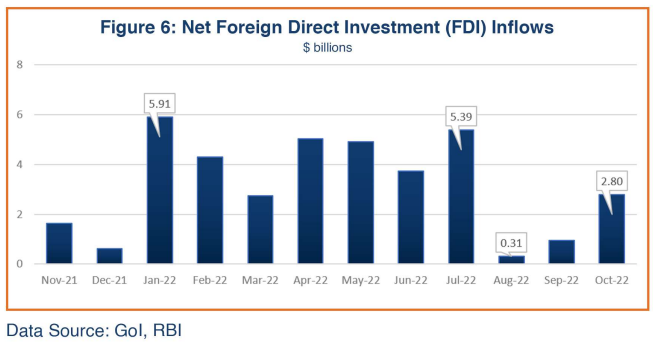

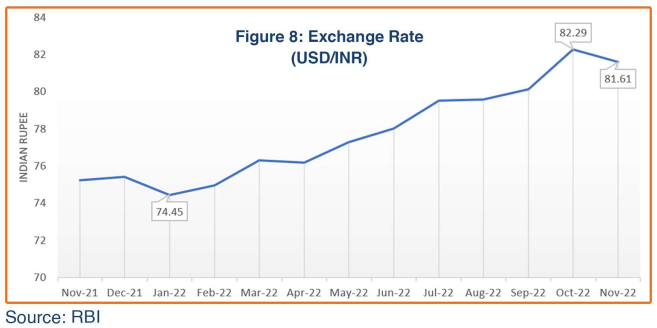

Despite volatile global recessionary trends, Indian exports posted 7.4% sequential growth in November 2022; future export performance will depend upon the degree and the length of the global economic slowdown. Imports slightly fell to $55.9 billion in November 2022 as the international prices of oil and fertilizers dropped, which eased the trade deficit to $23.9 billion from $26.9 billion in the previous month. Net FDI inflows in October 2022 (latest available data) rose significantly from the previous month to $2.8 billion. India’s foreign exchange reserves recovered significantly to $561 billion by the end of November and the Indian rupee strengthened to 81.61 against the US Dollar, from 82.29 in the previous month.

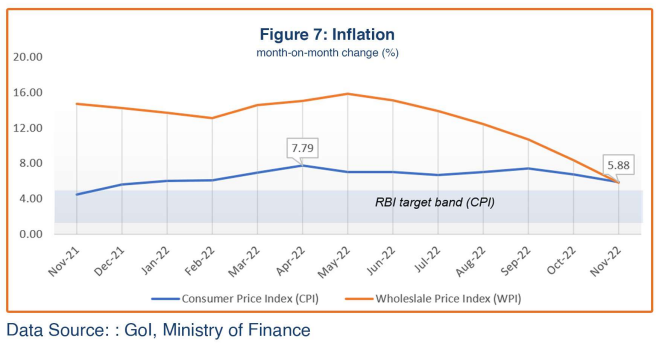

Lower food prices helped bring the consumer price index (CPI) down to 5.88% in November 2022 from the previous month’s 6.77%, falling below the 6.0% RBI target ceiling for the first time in 11 months. The RBI has kept its forecast of 6.7% retail inflation for fiscal year 2022-23 due to persisting food price pressures and global risks to costlier imports. The wholesale price index (WPI) dropped to two-year low of 5.85% in November from 8.39% in the previous month. The narrow gap between the CPI and WPI should push down retail inflation further in coming months.

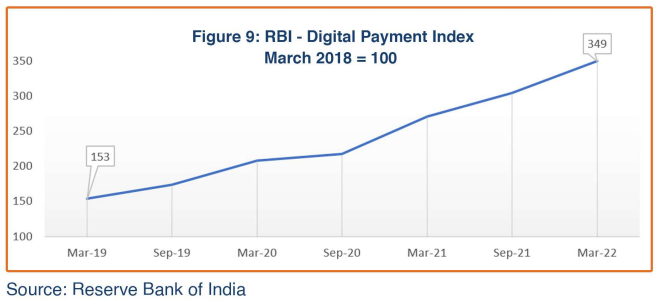

The RBI-Digital Payment Index (RBI-DPI) has shown rising trends over the last four years, which means that usage of digital payments is rising in India that will further improve faster liquidity flow in the market, cutting down the cash flow management.

The Government of India recently released India’s GDP growth numbers for the second quarter of the current fiscal year, according to which the GDP growth rate slowed down to 6.3% from 8.4% recorded the previous year. The strong performances in the services and farm sectors drove GDP growth in July-September quarter, but weaker performance in the manufacturing sector impacted overall growth. These trends suggest an uneven economic recovery in India post-COVID.

While India has shown a reasonable resilience to the recent supply disruptions, its near-term economic growth outlook remains unpredictable due to continuing geopolitical tensions, volatile currencies, and toughening global trade conditions amid rising inflation and recession. Due to the uncertain global conditions, the RBI, the ADB, the IMF and World Bank all project India’s FY2022-23 GDP growth in the range of 6.8% to 7%.

Demand Recovery Trends

Retail sales in November 2022 showed an uptrend in consumption demand; while vehicle sales were down 5% from the previous month due to seasonality and moderating exports, auto companies have hailed the sales of passenger vehicles despite the inflated costs of auto loans and long-term insurance premiums. India’s festive and wedding season in Q4 is well known to rack up some of the best sales results in the year. RBI reported healthy growth in bank credit at 17.2% at the end of November, compared with 17% a month ago, even though the cost of credit remains high due to the liquidity tightening by the RBI. The monthly survey by the Retailers Association of India (RAI) reported 15% higher sales during November compared to the pre-pandemic sales recorded for November 2019. With easing consumer inflation, retailers reported higher sales for consumer durables/electronics as well as for hotel/restaurant sales. A sustained rise in retail and passenger vehicle sales during the first seven months of the current fiscal year suggests domestic demand will dominate, which will have a multiplier effect on overall economic growth in India.

Supply Side Dynamics

Input Purchases

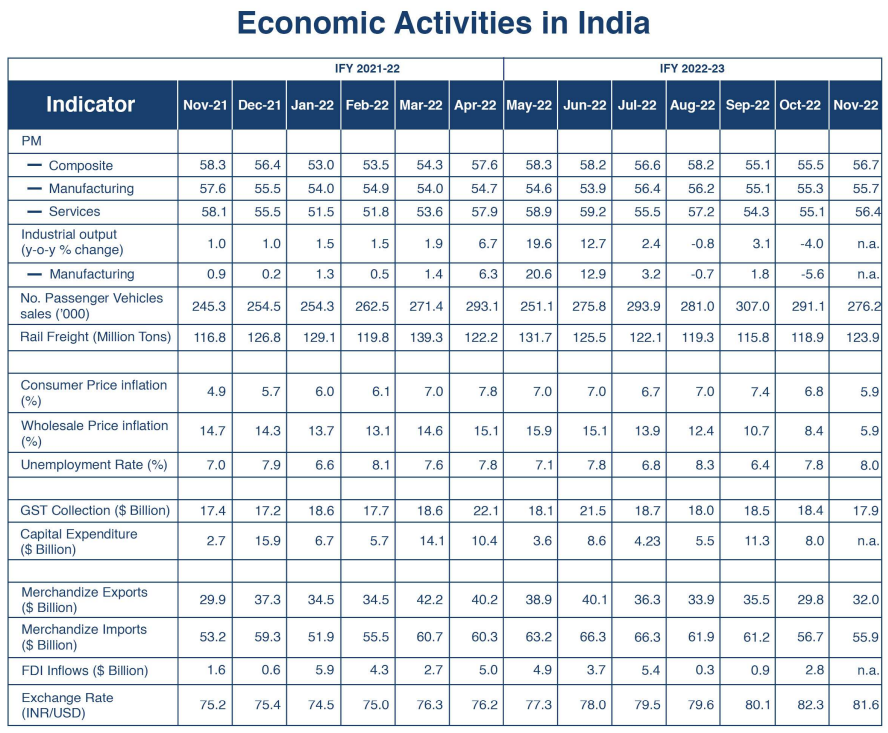

The overall business sentiment in November 2022 was stronger than the previous month. The November Composite Markit Purchase Managers Index (PMI) accelerated to 56.7 from 55.5 in October, reaffirming the expanding economic activities (Figure 1). A PMI above 50 reflects the optimistic mood of businesses that have made bold input purchases in anticipation of increased demand. The Services index rose to 56.4 from 55.1 and the Manufacturing PMI index was marginally up to 55.7 from the previous month’s 55.3 as inflation eased. These trends suggest a robust recovery in the service economy while the manufacturing sector recovers more slowly. According to S&P Global, factory activity was at a three-month high on the back of a two-year low in wholesale inflation, signaling resilience in demand despite worsening global economic conditions. The PMI Survey notes that monthly employment has risen at the second-quickest rate since January 2020, both in manufacturing and services.

Industrial Production

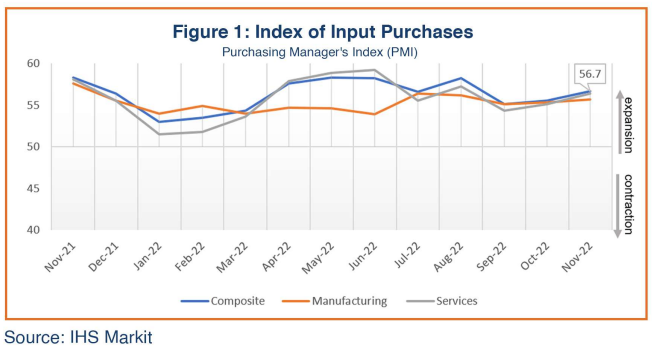

Total industrial production contracted 4% in October 2022, reversing the previous month’s 3.1% growth, on the back of a substantial decline in the manufacturing output (Figure 2). This is the first time in a year when industrial output recorded a significant negative growth. Growth across all segments got weaker compared to the previous month, generating a deceleration in the overall growth in industrial output. Manufacturing, which accounts for 77% of total industrial production, receded 5.6% year-on-year in October from 1.8% growth of the previous month; mining, which comprises 14% of total industrial output, rose only 2.5% compared with the growth of 4.6% year-on-year in September, and the growth rate in electricity production (8% of total industrial production), at 1.2%, was significantly down from the 11.6% growth achieved in the previous month. Capital goods production within the manufacturing sector showed a 10.3% growth in October 2022, hinting at remarkable growth in investments; the rate of growth was more than double the 10.3% of the previous month.

GST Revenues

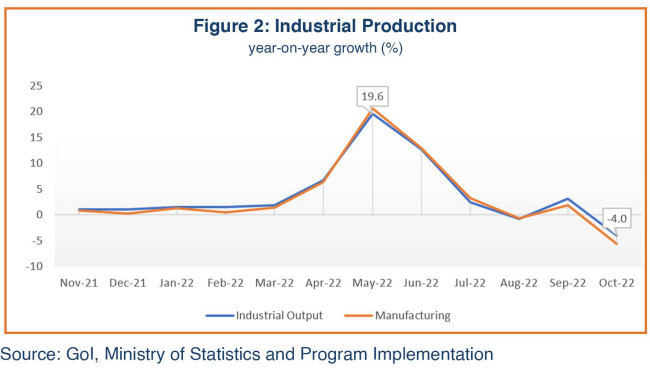

Changes in the value of Goods and Services Tax (GST) collection are an indicator of business transactions and increased rates and tax compliance. The GST collections have been ranging between $18 and $18.5 billion since the beginning of second quarter of the current fiscal year. The GST collections for November 2022 were pegged at $17.9 billion (Figure 3).

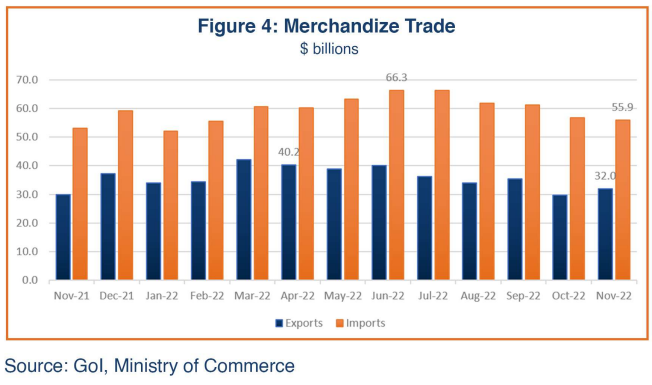

Trade

India’s merchandize exports rebounded 7.4% in November 2022 to $31.9 billion from the previous month’s $29.8 billion (Figure 4). India’s export performance for the first quarter of the current fiscal year was outstanding; however, the global recession, tightening liquidity in major economies to tame rising inflation, volatile currencies, and the resultant suppressed demand have impacted global trade negatively. Surpassing expectations, India’s exports in November performed well in commodity groups, such as electronic goods, gems and jewelry, readymade garments, drugs and pharmaceuticals, rice, leather & leather products, ceramic products & glassware, fruits and vegetables, processed food items, cereals, oil seeds, tobacco, and tea and coffee, despite the global economic slowdown.

According to the Ministry of Commerce, India has received a positive response to its recent initiative allowing local currency in international trade settlements. India has also removed the 15% export duty on steel that impacted the performance of engineering item exports when there is relatively lower demand for such products due to lesser economic activities globally. Export of high-volume chemical inputs and plastics are impacted, due to a lower demand and lower price realization from traditional export markets and higher domestic industry demand.

India’s merchandize imports are estimated around $55.9 billion in November, declining 1.4% from $56.7 billion in the previous month. Imports are generally directly related to industrial activity and a slight decline in imports is attributed to the softening international prices of fuel and fertilizers. India remains a major importer of fuel to fill increasing domestic demand-supply gap. That said, India’s import bill remains a cause of concern despite accelerated global monetary tightening measures.

Even though exports grew faster than imports decelerated in November 2022, the merchandize trade deficit at $24 billion remains a cause for concern as the high current account deficit (CAD) can impact the macroeconomic balance, putting pressure on the value of domestic currency.

Government Spending

Capital expenditure growth has been moderating since the beginning of the current fiscal year, though an uptick was visible in September (Figure 5 – latest available data). The finance minister has recently reaffirmed her Ministry’s claim to meet the fiscal deficit target of 6.4% of GDP in 2022-23, asserting that there is no fear of stagflation. The government has repeated that it will continue to focus on increasing capital expenditure while reducing revenue expenditure.

Foreign Direct Investment (FDI)

Foreign direct investment (FDI) equity flows showed mixed trends throughout the previous fiscal year. According to the latest data released by the Department of Industrial Policy and Internal Trade (DPIIT), in FY2021-22, FDI equity contracted marginally, by 1%, to $58.8 billion. However, total foreign direct investment (including equity inflows, reinvested earnings, and other capital) into India rose by 2%, peaking at $83.7 billion in FY2021-22. The first month of the new fiscal year 2022-23 (April 2022) witnessed India attracting $5 billion in total FDI inflows, followed by $4.92 billion in May and $3.74 billion in June. Net FDI peaked in July at $5.39 billion before falling significantly in August and September (Figure 6 – latest available data). Total net FDI into India expanded more than 17% to $13.61 billion in the first quarter of FY2022-23 compared to $11.55 billion for the corresponding period of the previous year.

Inflation

The overall inflation trajectory remains unstable given the continuing uncertainties in international commodity prices. The consumer price index (CPI) further moderated to 5.88% in November 2022 from 6.77% recorded in October, slipping below the RBI’s upper safety band of 6.0% for the first time in eleven months (Figure 7). The drop in CPI was mainly due to a more-than-expected fall in food prices, which account for about 40% share in the country’s CPI. Despite the continuing supply chain disruptions owing to ongoing geopolitical factors, prices were lower due to the usual seasonal changes in food prices, but non-food inflation was still above 6%. The RBI continues to give priority to price stability, stating that it will remain focused on the evolving inflation dynamics and projects inflation to remain above 4% for the next year. The RBI has raised the benchmark repo rate by 225 basis points since May to 6.25%, aimed at curbing consumer inflation.

Wholesale Price inflation in November dropped substantially to 5.85% from 8.39% in October, the lowest level in about two years, mainly due to a broad-based growth in manufacturing and services. Business sentiment is expected to improve following the softening of input prices. The RBI has flagged that the narrowing gap between wholesale and retail inflation implies a lower magnitude of pass-through of input costs on future retail inflation.

Foreign Exchange

India’s foreign reserves were estimated at $561 billion at the end of November 2022, gaining approximately $30 billion from the end of October. Until September 2022, the RBI had intervened intermittently in the foreign exchange market for liquidity management, including the selling of dollars, to manage depreciation in the Indian rupee, which resulted in a reduction of foreign exchange reserves. Foreign capital outflows and higher international prices also contributed to slumping foreign exchange reserves and depreciation of the rupee. In November the rupee touched a low point of 81.72/USD and averaged 81.61/USD for the month, down from the year’s low point of 82.29/USD recorded for October 2022 (Figure 8). The slight recovery in the rupee is due to restored sentiment in foreign fund inflows in capital markets. The RBI in June 2022 announced its decision to allow global trade in rupees; that may have also helped improve foreign exchange reserves.

Digital Payments

India is working toward becoming a cashless society, with consumers adopting online payment methods. The continuous rise in RBI Digital Payment Index (RBI-DPI) reveals an increasing trend in digital payments over the last four years, and observers expect it to continue its growth trajectory (Figure 9). Expanding digital payments will improve liquidity flow in the market, cutting the time and expense of cash flow management.

The RBI formulated the DPI to assess the extent of digital payment operations across India. Published with a lag of four months, the RBI-DPI includes a variety of payment parameters: enablers (such as Internet, mobile, bank accounts, Aadhaar, traders etc.), demand and supply infrastructure (such as credit/debit cards, mobile/Internet banking, bank branches, business correspondents, ATMs, QR codes, and intermediaries), performance (such as volume and value of digital payments, cash withdrawals, unique users, currency in circulation etc.) and consumer centricity (awareness and education, declines, complaints, frauds, and system downtime).

Economic Outlook

The second quarter (July-September 2022) GDP growth rate in India slowed to 6.3% from 8.4% recorded in the corresponding period of the previous year (Figure 10). Services (i.e., internal trade, hotel, transports, financial, real estate, and public administration) and the farm sector led the growth in GDP amidst rising interest rates and slowing manufacturing output, pointing to an uneven post-COVID recovery. Remarkable recovery in domestic demand balanced moderating exports due to global recession. India posted an impressive 13.5% growth for April-June 2022 quarter. Businesses ramped up capacity as domestic demand continued to recover during the second quarter of the fiscal year, but continuing supply disruptions, geopolitical challenges, high commodity prices, and a weaker rupee weathered their profitability. On the positive side, the government extended its capital expenditure by more than 49% in the first two quarters of the current fiscal year, compared to the corresponding period of the previous year; however, external trade performance reflected the negative impact of global recession and persisting inflationary pressure.

Most agencies have revised downward their forecasts of annual Indian GDP growth in FY2022-23. RBI and the Asian Development Bank (ADB) both project India’s growth at 7.0% while the International Monetary Fund (IMF) forecasts 6.8% growth on account of extended geopolitical tensions and an aggressive monetary policy tightening globally. Meanwhile, the World Bank has recently revised its growth forecast up slightly, to 6.9% from its earlier projection of 6.5%, on account of stronger consumption and increased domestic economic activities. In explaining the revision, the World Bank’s Country Director in India noted, “India’s economy has been remarkably resilient to the deteriorating external environment, and strong macroeconomic fundamentals have placed it in good stead compared to other emerging market economies.”

Businesses in India had hoped that softening international prices of fuel, fertilizers, and edible oils would help increase their profitability; however, the high input prices throughout the second quarter of the fiscal year proved detrimental. Nevertheless, now the reducing gap between input prices and consumer prices will send positive signals to the business community and lift both demand sentiment and output levels. Industrial and manufacturing output have shown sluggish growth and that remains an area of concern. The continuing volatility in global inflation management, as well as the slumping exports, will also make a significant difference in the performance of the economy, and India’s economic growth outlook in the coming months will likely be struggling with a widening trade deficit amid recession in advanced economies.

Major economies around the world, including India, face challenges from currency depreciation and the impact of global recession, but the Indian policymakers have voiced confidence India can weather the challenges because of its stronger financial sector, rising private capital expenditure, better control on inflation, and reviving foreign exchange reserves. The government expects around $40 billion worth FDI for the current fiscal year. Nonetheless, India’s economic growth outlook remains uncertain and will depend on private investment expenditure and the magnitude and length of the global recession.